Recent News & Event

Business Plans

At the heart of starting a business process lies the business plan, a dynamic document...

Business plan writers play a pivotal role in transforming entrepreneurial visions into tangible realities. Let...

Crafting a winning pitch deck that captivates investors is an art form, a delicate balance...

Introduction Let us discover the method of writing a Food Truck Business Plan. So, you’ve...

Daycare Business Plan Starting a daycare business is a rewarding venture, providing quality care for...

It is not easy to start your own business. Many people start their enterprises without...

Having a solid plan always pays off in the long run. Especially if it is...

Nowadays, eco-consciousness is not just a trend bu it has become a necessity, an emphasis...

A Case Study of How Strategic Financial Planning Led a Small Business to Success Our...

In the dynamic landscape of online commerce, having a robust E-commerce Business Plan is akin...

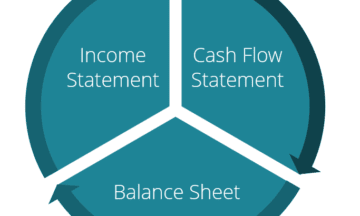

Here’s a simplified guide to understanding financial statements.Financial statements are like the health reports of...

Creating an effective financial management checklist for small businesses is crucial for the success and...